आजकल डिजिटल पेमेंट्स हमारी जिंदगी का हिस्सा बन चुके हैं। चाहे grocery shopping हो या ऑनलाइन बिल पेमेंट, UPI (Unified Payments Interface) ने cashless transactions को super easy बना दिया है।

लेकिन, अब Digital Rupee (e₹), यानी भारत का Central Bank Digital Currency (CBDC), भी चर्चा में है। Reserve Bank of India (RBI) ने इसे 2022 में pilot project के तौर पर launch किया था।

सवाल यह है: Digital Rupee और UPI में क्या अंतर है? और आपके लिए कौन सा better है? 🤔

इस article में हम Digital Rupee vs UPI में तुलना benefits, Examples, comparison table, और actionable tips के साथ करेंगे, चलिए शुरू करते हैं!

Page Contents

Digital Rupee (e₹) क्या है?

Digital Rupee भारत का official digital currency है, जिसे RBI issue और regulate करता है।

यह physical cash (नोट और सिक्के) का डिजिटल version है और legal tender माना जाता है।

इसे digital wallet में store किया जाता है, और आप इसका use peer-to-peer या merchant payments के लिए कर सकते हैं।

Digital Rupee की मुख्य विशेषताएं

- RBI-Backed: 100% safe और trusted, क्योंकि RBI इसे issue करता है।

- Digital Cash: Physical rupees की तरह ही value (1 e₹ = 1 ₹)।

- No Bank Intermediary: Transactions direct wallet-to-wallet होते हैं।

- Offline Capability: कुछ cases में internet के बिना भी use हो सकता है।

- Transparency: हर transaction traceable, जिससे black money और tax evasion कम होता है।

Example: अगर आपके digital wallet में 500 e₹ हैं, तो आप इसे direct किसी shopkeeper के wallet में transfer कर सकते हैं, बिना bank account के।

UPI क्या है?

UPI (Unified Payments Interface) एक real-time payment system है, जिसे National Payments Corporation of India (NPCI) ने develop किया।

यह bank accounts को link करके instant money transfer allow करता है।

Apps जैसे Google Pay, PhonePe, और Paytm ने UPI को super popular बना दिया।

UPI की मुख्य विशेषताएं

- Instant Transfers: Bank account से account में seconds में पैसे transfer।

- Multiple Apps: Google Pay, PhonePe, BHIM, आदि से use कर सकते हैं।

- Bank-Dependent: Transactions bank के through routed होते हैं।

- No Digital Currency: Physical cash का digital transfer, न कि currency।

- Widespread Use: QR codes, online shopping, और peer-to-peer payments के लिए ideal।

Example: अगर आप PhonePe से ₹500 किसी friend को भेजते हैं, तो पैसा आपके bank account से उनके bank account में चला जाता है।

Digital Rupee vs UPI: Detailed Comparison

| Feature | Digital Rupee (e₹) | UPI |

| Nature | Digital currency (legal tender) | Payment platform (bank account transfer) |

| Issuer | RBI | NPCI |

| Operation | Wallet-to-wallet, no bank intermediary | Bank-to-bank, intermediary needed |

| Transaction Speed | Instant (direct) | Instant (bank-routed) |

| Offline Use | Possible in some cases | Internet mandatory |

| Safety | 100% safe (RBI-backed) | Safe, but bank security-dependent |

| Use Cases | Retail, cross-border, government transfers | Peer-to-peer, merchant payments, online shopping |

| Cost | Low (no intermediaries) | Low, but bank charges possible |

| Traceability | High (reduces black money) | Moderate (bank records) |

Digital Rupee vs UPI: Major Differences

| Feature | Digital Rupee (e₹) | UPI |

| Currency vs Platform | यह खुद एक currency है, जैसे physical ₹100 का नोट, लेकिन digital form में। | यह एक platform है, जो bank accounts के बीच पैसे transfer करता है। |

| Bank Involvement | No bank intermediary। पैसा आपके digital wallet से direct recipient के wallet में जाता है। | Bank account से account में transfer, bank middleman की तरह काम करता है। |

| Offline Capability | कुछ cases में offline transactions possible है, खासकर rural areas में। | Internet connection जरूरी है। |

| Use Cases | Everyday retail, government benefit transfers (DBT), और cross-border payments के लिए ideal है। | Peer-to-peer, merchant payments, और online shopping के लिए popular है। |

| Cost Efficiency | No intermediaries, तो transaction cost कम है। | Bank charges apply हो सकते हैं, लेकिन usually free होता है। |

Example:

अगर आप shopkeeper को ₹1,000 pay करते हैं:

Digital Rupee: आपके e₹ wallet से shopkeeper के wallet में direct transfer होता है।

UPI: आपके bank account से shopkeeper के bank account में transfer होता है।

Digital Rupee vs UPI: कौन सा चुनें?

आपके लिए सही option आपके needs पर depend करता है:

Digital Rupee चुनें अगर :

- आप direct, bank-free transactions चाहते हैं।

- आपके area में internet connectivity limited है।

- आप government benefits या cross-border payments के लिए solution ढूंढ रहे हैं।

- आप high transparency और low transaction cost prefer करते हैं।

Example: अगर आप rural area में हैं और internet slow है, तो Digital Rupee wallet से offline payment आसान है।

UPI चुनें अगर:

- आप instant bank transfers चाहते हैं।

- आप already Google Pay, PhonePe जैसे apps use करते हैं।

- आप merchant payments (जैसे shops, online stores) ज्यादा करते हैं।

- आप user-friendly interface और widespread acceptance prefer करते हैं।

Example: Online shopping या friend को quick payment के लिए UPI best है।

Actionable Tip: दोनों का combination use करें – daily small payments के लिए UPI और long-term savings या offline payments के लिए Digital Rupee wallet।

Digital Rupee vs UPI: चुनने से पहले विचार करने योग्य बातें

- Availability: Digital Rupee अभी pilot phase में है (Mumbai, Delhi, Bengaluru, आदि)। UPI nationwide popular है।

- Ease of Use: UPI apps user-friendly हैं। Digital Rupee के लिए wallet setup और KYC जरूरी

- Acceptance: UPI merchants और individuals में widely accepted। Digital Rupee अभी limited merchants तक।

- Security: Digital Rupee RBI-backed, 100% safe। UPI bank security पर depend करता है।

- Future Scope: Digital Rupee cross-border और government schemes में game-changer हो सकता है। UPI domestic payments में king है।

Example: अगर आप abroad से payment receive करना चाहते हैं, तो Digital Rupee जो future में easy हो सकता है। Daily small transactions के लिए UPI अभी best है।

Common Myths About Digital Rupee and UPI

| Myth | Truth |

| Digital Rupee और UPI same हैं। | Digital Rupee एक currency है, UPI एक payment platform। |

| Digital Rupee risky है। | RBI-backed, तो 100% safe। |

| UPI offline work करता है। | UPI को internet चाहिए, Digital Rupee offline possible। |

Actionable Tips for Users

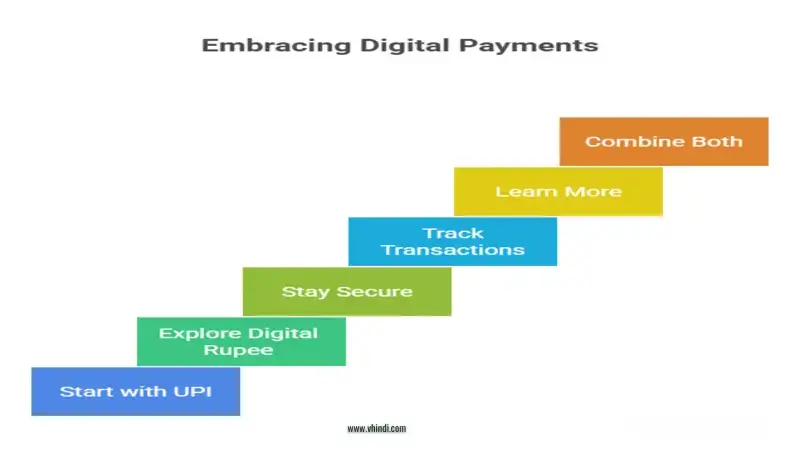

- Start with UPI: Google Pay, PhonePe, या BHIM download करें और daily payments शुरू करें।

- Explore Digital Rupee: Pilot cities (Mumbai, Delhi) में RBI-approved banks से digital wallet setup करें।

- Stay Secure: UPI PIN और wallet security strong रखें। Suspicious apps avoid करें।

- Track Transactions: Digital Rupee की traceability से black money avoid करें। UPI history check करें।

- Learn More: RBI website पर Digital Rupee updates और NPCI पर UPI guidelines पढ़ें।

- Combine Both: Small payments के लिए UPI, government benefits या offline use के लिए Digital Rupee।

Conclusion

Digital Rupee (e₹) और UPI दोनों ही India के digital payment revolution का हिस्सा हैं, लेकिन उनके purposes अलग हैं।

Digital Rupee एक digital currency है, जो direct, bank-free transactions और offline capability देता है वही UPI एक fast, bank-linked payment platform है, जो daily transactions के लिए super convenient है।

आपके लिए सही option आपके use case पर depend करता है – small, instant payments के लिए UPI और future-focused, offline-capable transactions के लिए Digital Rupee।

Digital Rupee और UPI दोनों India की cashless economy को boost कर रहे हैं। UPI अभी daily use के लिए king है, लेकिन Digital Rupee future में cross-border और offline payments में revolution ला सकता है।

दोनों को समझें, और अपने financial goals के हिसाब से smartly use करें।

Call to Action: आज ही PhonePe या Google Pay से UPI शुरू करें। Digital Rupee pilot में interested हैं, तो SBI, ICICI जैसे banks से contact करें और digital wallet setup करें।

Cashless India का हिस्सा बनें।

People also ask :

Digital Rupee (e₹) सीधे RBI द्वारा जारी किया गया है, इसलिए यह फिजिकल कैश जितना ही 100% सुरक्षित है। UPI की सुरक्षा आपके बैंक के सिक्योरिटी सिस्टम पर निर्भर करती है, हालांकि यह भी बहुत सुरक्षित है।

नहीं, Digital Rupee (e₹) wallet-to-wallet काम करता है, इसलिए ट्रांजैक्शन के लिए बैंक अकाउंट की ज़रूरत नहीं है। इसके विपरीत, UPI के हर ट्रांजैक्शन के लिए एक लिंक किया हुआ बैंक अकाउंट होना अनिवार्य है।

सबसे बड़ा अंतर यह है कि Digital Rupee (e₹) खुद पैसा (एक डिजिटल करेंसी) है, जिसे RBI जारी करता है। वहीं, UPI सिर्फ बैंक अकाउंट से पैसा भेजने का एक तरीका (पेमेंट प्लेटफॉर्म) है।

नहीं, ऐसा होने की संभावना कम है क्योंकि दोनों के उद्देश्य अलग-अलग हैं। UPI रोज़मर्रा के बैंक-आधारित पेमेंट्स के लिए बना रहेगा, जबकि Digital Rupee (e₹) कैश का एक डिजिटल विकल्प और ऑफलाइन पेमेंट्स जैसे नए उपयोगों पर केंद्रित होगा।

हाँ, RBI, Digital Rupee (e₹) को ऑफलाइन पेमेंट के लिए भी विकसित कर रहा है, जिससे यह बिना इंटरनेट वाले इलाकों में भी काम कर सकेगा। UPI को काम करने के लिए हमेशा एक एक्टिव इंटरनेट कनेक्शन की ज़रूरत होती है।