क्या आपने कभी सोचा कि अचानक जरूरत पड़ने पर, जैसे मेडिकल इमरजेंसी, जॉब loss, या गाड़ी की repair – आपके पास तुरंत पैसा कहां से आएगा?

यही है Emergency Fund की जरूरत।

Emergency fund आपके financial safety net की तरह है, जो आपको unexpected situations में support करता है।

लेकिन सवाल यह है: इस पैसे को savings account में रखें या liquid fund में? 🤔

अगर आप अपना emergency fund सही जगह रखना चाहते हैं और चाहते हैं कि आपकी savings हमेशा safe, accessible और growth के साथ रहें, तो यह article आपके लिए है।

यहाँ हम discuss करेंगे best savings account in India, liquid funds vs fixed deposit, tax on liquid funds और emergency fund के लिए best liquid funds कौन-से हैं – ताकि आप अपने पैसे को smart तरीके से manage कर सकें और high interest savings account in India जैसी options का फायदा उठा सकें।

जानें emergency fund vs fixed deposit की reality, कहाँ emergency fund रखना best रहेगा (where to keep emergency fund), और कैसे अपने financial future को secure रखें।

Page Contents

Emergency Fund क्या है और क्यों जरूरी है?

Emergency fund वह पैसा होता है, जो आप unexpected expenses के लिए अलग रखते हैं।

Experts recommend करते हैं कि 6-12 months के living expenses (जैसे rent, bills, groceries) का emergency fund होना चाहिए।

Example: अगर आपका monthly खर्च ₹20,000 है, तो ideal emergency fund ₹1.2 लाख से ₹2.4 लाख होना चाहिए।

लेकिन इस पैसे को कहां रखें?

Savings account safe और easily accessible है, लेकिन returns कम देता है। Liquid funds थोड़े ज्यादा returns देते हैं, लेकिन क्या वे safe हैं?

आइए दोनों को compare करें।

Savings Account: Features और Benefits

Savings account हर किसी के लिए जाना-पहचाना option है। यह banks में available होता है और emergency fund के लिए popular है।

Key Features of Savings Account:

- Interest Rate: 3-6% per annum (बैंक के हिसाब से)।

- Liquidity: Instant access – ATM, net banking, या UPI से तुरंत withdraw कर सकते हैं।

- Safety: 100% safe, DICGC insurance के तहत ₹5 लाख तक की रकम protected।

- Minimum Balance: कुछ banks में ₹1,000-₹10,000 minimum balance जरूरी।

- Accessibility: 24/7 access via mobile banking, debit card, या branch।

- Tax: Interest पर tax लगता है अगर yearly interest ₹40,000 से ज्यादा हो (senior citizens के लिए ₹50,000)।

Example: अगर आप ₹1 लाख savings account में रखते हैं (4% interest), तो 1 साल बाद आपको ₹1.04 लाख मिलेंगे। लेकिन inflation (6-7%) की वजह से real value कम हो सकती है।

Savings account के Pros:

- Instant withdrawal, no waiting period।

- Zero risk, government-backed।

- Easy to manage, no market knowledge needed।

Savings account के Cons:

- Low returns (3-6%), inflation को beat नहीं करता।

- Minimum balance penalties हो सकते हैं।

अगर आप high interest savings account in India ढूंढ रहे हैं, तो Kotak 811, IDFC First, और SBI Savings Account जैसे options consider कर सकते हैं, जहाँ आपको 5-7% तक interest मिलता है।

High interest savings account की liquidity और instant access आपको emergency time में help करेगा, जबकि कुछ accounts में minimum balance requirement हो सकती है।

Liquid Fund: Features और Benefits

Liquid funds एक type के mutual funds हैं, जो short-term, low-risk investments (जैसे government securities, treasury bills) में पैसा लगाते हैं। ये emergency fund के लिए good alternative हो सकते हैं।

Key Features of Liquid Fund:

- Interest Rate: 6-7.5% per annum (market-dependent, थोड़ा fluctuate कर सकता है)।

- Liquidity: High liquidity – redemption request पर 1-2 days में पैसा account में।

- Safety: Very low risk, क्योंकि short-term, high-quality securities में invest करते हैं।

- Minimum Investment: ₹500 से शुरू कर सकते हैं (SIP या one-time)।

- Tax: Short-term capital gains (less than 3 years) पर income tax slab rate लागू। Long-term (3+ years) पर 20% with indexation।

- Accessibility: Online platforms (Groww, Zerodha) या mutual fund houses के जरिए invest/withdraw।

Example: ₹1 लाख liquid fund में (7% return) 1 साल बाद ~₹1.07 लाख बन सकता है। Redemption में 1-2 दिन लगते हैं।

Liquid fund के Pros:

- Higher returns than savings account (6-7.5%)।

- Low risk, almost as safe as savings account।

- No minimum balance requirement।

Liquid fund के Cons:

- 1-2 days का withdrawal time।

- थोड़ा market risk (हालांकि very low)।

- Mutual fund knowledge की थोड़ी जरूरत।

अगर सवाल है best liquid funds for emergency fund in India, तो कुछ popular options हैं:

- HDFC Liquid Fund,

- ICICI Pru Liquid Fund,

- Axis Liquid Fund,

- SBI Liquid Fund,

- Aditya Birla SL Liquid Fund।

इन funds का exit load negligible है और returns stable रहते हैं, जिससे emergency fund का value inflation के सामने कम नहीं होता हैं।

Savings Account vs Liquid Fund: Detailed Comparison

| Feature | Savings Account | Liquid Fund |

| Interest Rate | 3-6% | 6-7.5% |

| Liquidity | Instant (ATM/UPI) | 1-2 days |

| Safety | 100% safe (DICGC insured) | Very low risk (market-linked) |

| Minimum Investment | ₹0-₹10,000 (bank-dependent) | ₹500 |

| Tax on Returns | Interest taxable (>₹40,000/year) | Short-term gains taxable (slab rate) |

| Best For | Instant access, zero risk | Higher returns, short-term parking |

| Accessibility | Bank branch, ATM, net banking | Online platforms, mutual fund apps |

Savings Account vs Liquid Fund: कौन सा चुनें?

Emergency fund के लिए सही option आपके needs पर depend करता है। चलिए, इसे और clear करते हैं:

Savings Account चुनें अगर:

- आपको instant access चाहिए (जैसे medical emergency में same-day withdrawal)।

- आप zero risk चाहते हैं और market fluctuations से बचना चाहते हैं।

- आप simple, no-hassle option prefer करते हैं।

- आप small amount (₹50,000 तक) रखना चाहते हैं।

Example: अगर आपका emergency fund ₹50,000 है और आपको तुरंत access चाहिए, तो savings account best है।

Liquid Fund चुनें अगर:

- आप higher returns (6-7.5%) चाहते हैं और 1-2 दिन का wait afford कर सकते हैं।

- आपका emergency fund बड़ा है (₹1 लाख+) और आप inflation को beat करना चाहते हैं।

- आप थोड़ा mutual fund knowledge सीखने को तैयार हैं।

- आप long-term emergency fund (3-6 months) के लिए invest कर रहे हैं।

Example: अगर आप ₹2 लाख का emergency fund बनाना चाहते हैं और 1-2 दिन का withdrawal time ठीक है, तो liquid fund में 7% return से ज्यादा growth मिलेगा।

Actionable Tip: Emergency fund को split करें, इसके लिए Stair-Step Approach का उपयोग कर सकते है :

- Step 1 (पहला goal – immediate security): सबसे पहले, अपना पूरा ध्यान केवल Savings Account पर लगाएं और उसमें कम से कम 1 महीने के खर्च के बराबर रकम जमा करें। यह आपका ‘immediately ready‘ fund है।

- Step 2 (दूसरा goal – growth): जब आपका पहला goal पूरा हो जाए, तब अगले 3-5 महीनों के खर्च के बराबर की रकम Liquid Fund में जमा करना शुरू करें। इससे आपको बेहतर रिटर्न मिलेगा।

इस तरह, आप पहले अपनी तत्काल सुरक्षा सुनिश्चित करते हैं और फिर अपने फंड को ग्रोथ के लिए ले जाते हैं। यह तरीका मानसिक रूप से बहुत आसान और motivating होता है।

Things to Consider Before Choosing

दोनों options में invest करने से पहले इन points का ध्यान रखें:

- Accessibility Needs: Medical या urgent expenses के लिए savings account better है। Non-urgent needs के लिए liquid fund।

- Fund Size: Small fund (₹50,000 तक) के लिए savings account, large fund (₹1 लाख+) के लिए liquid fund।

- Risk Tolerance: Market में थोड़ा risk ले सकते हैं तो liquid fund, zero risk चाहिए तो savings account।

- Tax Implications: Liquid fund में short-term gains पर higher tax लग सकता है (high income slab वालों के लिए)।

- Platform: Liquid fund के लिए trusted platforms (Groww, Zerodha) चुनें और low expense ratio funds select करें।

Example: अगर आप ₹1.5 लाख का emergency fund बनाते हैं, तो ₹75,000 savings account में (4% interest) और ₹75,000 liquid fund में (7% return) रखें। 1 साल बाद total ~₹1.56 लाख हो सकता है।

Common Myths About Emergency Funds

| Myth | Truth |

| Emergency fund को fixed deposit में रखना चाहिए। | FD में lock-in period होता है, जो emergency में problem create कर सकता है। |

| Liquid funds risky हैं। | Liquid funds very low risk होते हैं, क्योंकि short-term, high-quality securities में invest करते हैं। |

| Savings account में पैसा रखने से नुकसान होता है। | Inflation से value कम हो सकती है, लेकिन instant access और safety इसे emergency के लिए ideal बनाते हैं। |

Why This Decision Matters?

- Savings Account: Zero risk, instant access, लेकिन low returns (3-6%)।

- Liquid Fund: Higher returns, low risk, लेकिन 1-2 दिन का withdrawal time।

- Best Strategy: 50-50 split (savings + liquid fund) से safety और growth दोनों मिलते हैं।

- Key to Success: 6-12 months का emergency fund बनाएं और regular review करें।

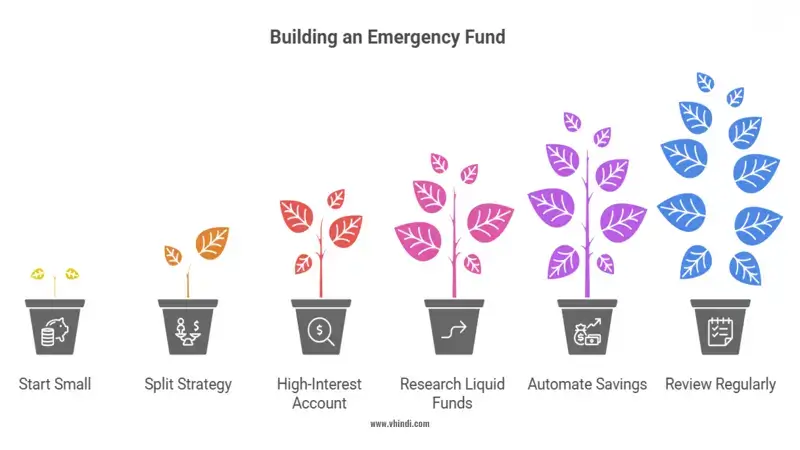

Actionable Tips for Emergency Fund

- Start Small: ₹10,000 से savings account में शुरू करें, फिर monthly add करें।

- Split Strategy: 50% savings account, 50% liquid fund (जैसे HDFC Liquid Fund, SBI Liquid Fund)।

- Choose High-Interest Savings Account: Kotak 811, IDFC First (up to 6%) जैसे banks चुनें।

- Research Liquid Funds: Low expense ratio और good track record वाले funds select करें (जैसे ICICI Prudential Liquid Fund)।

- Automate Savings: Monthly auto-transfer setup करें ताकि fund regularly बढ़े।

- Review Regularly: हर 6 महीने में fund size और returns check करें।

Conclusion

Emergency fund आपके financial plan का backbone है, और इसे सही जगह रखना बहुत जरूरी है।

Savings account instant access और 100% safety देता है, जो urgent needs के लिए perfect है। Liquid fund higher returns (6-7.5%) और low risk देता है, जो bigger funds और non-urgent needs के लिए ideal है।

दोनों के अपने फायदे हैं और सही choice आपके goals, accessibility needs और risk tolerance पर depend करता है।

Emergency fund आपकी financial security का base है। Savings account और liquid fund दोनों safe options हैं, लेकिन अपनी जरूरतों के हिसाब से choose करें।

अगर instant access priority है, तो savings account, अगर higher returns चाहिए, तो liquid fund और Best approach है, दोनों का combination.

आज ही शुरू करें और अपने future को secure करें।

Call to Action: अपने bank में high-interest savings account खोलें और ₹5,000 से emergency fund शुरू करें। Liquid fund के लिए Groww या Zerodha पर research करें और ₹500 से SIP शुरू करें।

Financial safety, अब दूर नहीं।

People also ask :

आजकल Kotak 811, IDFC First, और SBI जैसे high interest savings accounts सबसे ज्यादा popular हैं।

Liquid funds withdrawal में सिर्फ 1-2 days लगते हैं, returns भी FD से थोड़े ज्यादा होते हैं और short-term goals के लिए better हैं।

अगर liquid fund में investment less than 3 years है तो gains आपकी income tax slab से taxable हैं, 3 साल से ज्यादा हो तो 20% tax लगेगा + indexation benefit मिलता है। यानी long-term holding पर tax में थोड़ी राहत possible है।

Emergency fund की liquidity ज़रूरी है – FD में premature withdrawal पर penalty लगती है, whereas emergency fund को liquid fund या savings account में रखें तो instant या 1-2 days access मिलेगा।

Emergency fund को best high interest savings account या top liquid funds (like ICICI Pru, HDFC, SBI) में रखें ताकि पैसा safe रहे और instant या fast access मिले।

सबसे ज्यादा trusted liquid funds हैं: ICICI Prudential Liquid Fund, SBI Liquid Fund, HDFC Liquid Fund और Axis Liquid Fund।

इन funds में low risk, stable returns और fast withdrawal मिलता है। यह emergency fund के लिए ideal choice है।