हर पैरेंट चाहता है कि उनके बच्चों का भविष्य financially secure हो, चाहे वह higher education हो, foreign studies या उनकी शादी।

लेकिन सवाल यह है की इतने बड़े goals के लिए पैसे कैसे जुटाएं?

जवाब है Mutual Fund Portfolio.

Mutual funds बच्चों के लिए एक smart और flexible investment option हैं, जो छोटी रकम से शुरू करके लंबे समय में बड़ा फंड बना सकते हैं।

इस article में हम आपको बताएंगे कि बच्चों के लिए mutual fund portfolio कैसे बनाएं, कौन से funds चुनें और कैसे सही planning से आप उनके सपनों को हकीकत में बदल सकते हैं।

Page Contents

Mutual Fund Portfolio क्या है?

एक Mutual Fund Portfolio को एक ‘स्कूल टिफिन बॉक्स‘ की तरह समझिए। जिस तरह आप उसमें रोटी, सब्ज़ी, सलाद और फल रखते हैं ताकि बच्चे को पूरा nutrition मिले, उसी तरह Portfolio में अलग-अलग तरह के funds (Equity, Debt) रखे जाते हैं ताकि आपका investment संतुलित रहे और risk कम हो।

Mutual fund portfolio एक collection of investments है, जिसमें आप अलग-अलग types के mutual funds (equity, debt, hybrid) में पैसे लगाते हैं, ताकि risk कम हो और returns ज्यादा मिलें।

बच्चों के लिए portfolio बनाते समय focus उनके long-term goals (जैसे education, marriage) पर होता है, क्योंकि बच्चों की उम्र कम होती है, जिससे compounding का maximum benefit मिलता है।

Example: अगर आप अपने 5 साल के बच्चे के लिए हर महीने 5,000 रुपये का SIP शुरू करते हैं, और 15% average return मिले, तो 15 साल बाद (जब बच्चा 20 साल का होगा) आपका investment 24 लाख रुपये बन सकता है।

बच्चों के लिए Mutual Fund Portfolio बनाने के फायदे

Mutual funds बच्चों के लिए ideal हैं, क्योंकि:

- Long-Term Growth: बच्चों की उम्र कम होने से 10-20 साल की investment horizon मिलती है, जो compounding के लिए perfect है।

- Small Investments: 500 रुपये महीने से SIP शुरू कर सकते हैं, जो हर budget में fit होता है।

- Diversification: Equity, debt, और hybrid funds मिलाकर risk balance कर सकते हैं।

- Flexibility: Funds switch कर सकते हैं, SIP amount बढ़ा-घटा सकते हैं, या anytime withdraw कर सकते हैं।

- Professional Management: Fund managers आपके पैसे को smartly invest करते हैं, आपको market की knowledge की जरूरत नहीं।

Example: 10 साल तक 3,000 रुपये/month का SIP (12% return) आपको 7 लाख+ रुपये दे सकता है, जो बच्चे की college fees के लिए काफी हो सकता है।

बच्चों के लिए Mutual Fund Portfolio बनाते समय क्या ध्यान रखें?

Portfolio बनाना आसान है, लेकिन सही planning जरूरी है। ये हैं key points:

- Define Goals: बच्चे के लिए क्यों save करना चाहते हैं? जैसे education, marriage या foreign studies।

- Time Horizon: Goal कितने साल बाद है? 5, 10, या 15 साल? Longer horizon में equity funds बेहतर हैं।

- Risk Tolerance: बच्चों के लिए usually high risk ले सकते हैं, क्योंकि time ज्यादा होता है। लेकिन balance जरूरी है।

- Diversification: Equity, debt, और hybrid funds का mix बनाएं ताकि risk कम हो।

- Regular Review: हर 6-12 महीने में portfolio check करें और जरूरत पड़ने पर funds switch करें।

बच्चों के लिए Mutual Funds के प्रकार

| Fund Type | Risk Level | Expected Returns | Best for Time Horizon | Example Funds |

| Equity Funds | High | 12-15% | 7+ years | SBI Bluechip, Mirae Asset Large Cap |

| Debt Funds | Low | 6-8% | 1-5 years | HDFC Short Term Debt Fund |

| Hybrid Funds | Medium | 8-12% | 3-7 years | ICICI Prudential Balanced Advantage |

| Children’s Funds | Medium | 8-12% | 5-15 years | HDFC Children’s Gift Fund |

किसके नाम पर invest करें? – अपने या बच्चे के?

बच्चों के लिए Mutual Fund Portfolio बनाते समय एक common confusion यह होता है, कि invest किसके नाम पर किया जाए – बच्चे के या अपने?

यह एक ज़रूरी सवाल है क्योंकि दोनों ही तरीकों के अपने फायदे हैं। आपकी planning और comfort के हिसाब से आप कोई भी option चुन सकते हैं, लेकिन फैसला लेने से पहले दोनों को समझना ज़रूरी है।

बच्चे के नाम पर (In the Child’s Name as a Minor)

इसमें बच्चा folio का first and sole holder होता है, और parent या legal guardian account को operate करते हैं।

फायदे (Benefits):

- Dedicated Fund: यह पैसा पूरी तरह से बच्चे के future के लिए ‘lock’ हो जाता है। इससे एक financial discipline बनता है और आप इस पैसे को किसी और काम के लिए use करने से बचते हैं।

- Financial Literacy: जब बच्चा बड़ा होता है, तो आप उसे उसका portfolio दिखाकर financial planning सिखा सकते हैं।

ध्यान रखने वाली बातें (Things to Keep in Mind):

- बच्चे का Control: जैसे ही आपका बच्चा 18 साल का होता है, वह उस investment का legal owner बन जाता है। इसके बाद पैसे का इस्तेमाल कैसे करना है, यह पूरी तरह से उसका decision होगा।

- थोड़ी ज़्यादा Paperwork: इसके लिए बच्चे के documents (जैसे birth certificate) की ज़रूरत पड़ती है।

अपने खुद के नाम पर (In Your Own Name)

इसमें आप अपने ही Demat या mutual fund account में एक नया folio बनाते हैं और उसे mentally बच्चे के goal के लिए ‘tag’ कर देते हैं।

फायदे (Benefits):

- Full Control: Investment पर हमेशा आपका पूरा control रहता है, भले ही बच्चा 18 साल का हो जाए। आप यह ensure कर सकते हैं कि पैसा सही goal के लिए ही इस्तेमाल हो।

- Easy & Fast Process: इसके लिए किसी extra documents की ज़रूरत नहीं होती और process बहुत तेज़ होता है।

ध्यान रखने वाली बातें (Things to Keep in Mind):

- Discipline की ज़रूरत: क्योंकि पैसा आपके ही account में होता है, तो discipline की ज़रूरत होती है ताकि आप उसे किसी और इमरजेंसी के लिए use न कर लें।

कौन सा option बेहतर है?

यह पूरी तरह से आपकी प्लानिंग पर depend करता है।

- अगर आप एक dedicated fund बनाना चाहते हैं और यह सुनिश्चित करना चाहते हैं कि वह पैसा सिर्फ बच्चे के लिए ही रहे, तो बच्चे के नाम पर invest करना एक अच्छा option है।

- अगर आप पैसे पर full control रखना चाहते हैं ताकि उसका सही इस्तेमाल सुनिश्चित कर सकें, तो अपने नाम पर invest करना ज़्यादा safe option है।

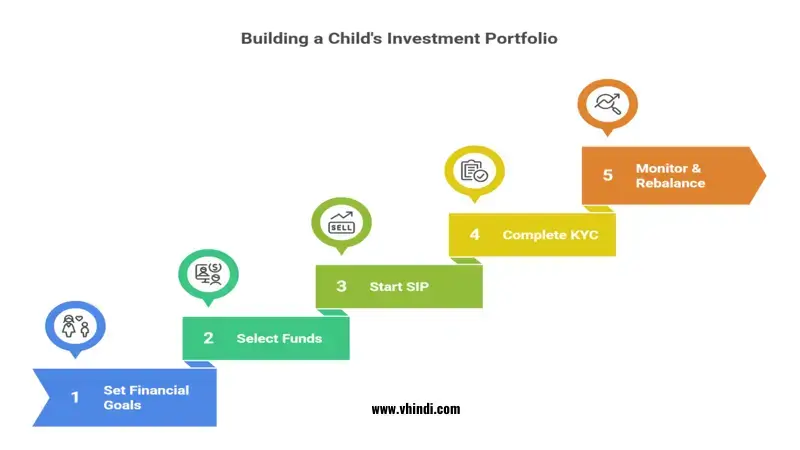

बच्चों के लिए Mutual Fund Portfolio बनाने के Steps

चलिए, step-by-step guide देखते हैं कि portfolio कैसे बनाएं:

- Set Financial Goals: Decide करें कि बच्चे के लिए क्यों save करना है।

Example: 15 साल बाद foreign education के लिए 20 लाख रुपये। - Choose Investment Amount: Monthly budget decide करें। 500 रुपये से भी शुरू कर सकते हैं।

- Select Funds: Goal और time horizon के हिसाब से funds चुनें:

- Long-Term (10+ years): 70% Equity, 20% Hybrid, 10% Debt।

- Medium-Term (5-10 years): 50% Equity, 30% Hybrid, 20% Debt।

- Short-Term (1-5 years): 60% Debt, 30% Hybrid, 10% Equity।

- Start SIP: Online platforms जैसे Groww, Zerodha या mutual fund websites पर account बनाएं और SIP start करें।

- Complete KYC: PAN, Aadhar, और bank details upload करें। Children’s funds में child का birth certificate भी लग सकता है।

- Monitor & Rebalance: हर साल portfolio review करें। अगर कोई fund underperform कर रहा हो, तो switch करें।

Best Mutual Funds for Children

कुछ popular funds जो बच्चों के लिए suitable हैं:

- HDFC Children’s Gift Fund: Balanced fund, education और marriage goals के लिए ideal।

Returns: ~10-12% (past 10 years)। - SBI Equity Hybrid Fund: Equity और debt का mix, long-term growth के लिए good।

Returns: ~12-14% (past 5 years)। - ICICI Prudential Equity & Debt Fund: Aggressive hybrid fund, medium risk।

Returns: ~11-13% (past 5 years)। - Aditya Birla Sun Life Tax Relief 96: ELSS fund, tax saving के साथ growth।

Returns: ~12% (past 5 years)।

Note: Past performance future returns की guarantee नहीं है। हमेशा fund का track record, expense ratio, और fund manager की history check करें।

Mutual Fund Portfolio के लिए Actionable Tips for Parents:

- Start Early: जितनी जल्दी SIP शुरू करेंगे, उतना ज्यादा compounding का फायदा।

Example: 5 साल के बच्चे के लिए 2,000 रुपये/month SIP (12% return) 18 साल बाद ~50 लाख बना सकता है। - Diversify Funds: Equity, debt, और hybrid funds का balance बनाएं।

- शुरुआत में 2-3 funds चुनें। Example:

- 60% in SBI Equity Hybrid Fund,

- 20% in Mirae Asset Large Cap, और

- 20% in HDFC Short Term Debt Fund।

- Use Children’s Funds: HDFC Children’s Gift Fund जैसे dedicated funds try करें।

- Increase SIP Amount: Income बढ़ने पर SIP रकम बढ़ाएं।

- Educate Yourself: Mutual fund apps (Groww, Zerodha) पर research करें या financial advisor से सलाह लें।

- Stay Consistent: Market fluctuations से घबराएं नहीं, regular SIP continue करें।

Common Mistakes to Avoid

Portfolio बनाते समय ये गलतियां avoid करें:

- Single Fund Dependency: सारा पैसा एक fund में न लगाएं, Diversify करें।

- Short-Term Thinking: Equity funds में 5-7 साल से कम समय के लिए invest न करें।

- Ignoring Inflation: Education costs हर साल 6-8% बढ़ते हैं। High-return funds चुनें।

- Stopping SIPs: Market गिरने पर SIP रोकना गलत है। Rupee cost averaging से फायदा मिलता है।

- Not Reviewing: Funds की performance regularly check न करना losses का कारण बन सकता है।

Conclusion

बच्चों के लिए mutual fund portfolio बनाना एक thoughtful और powerful step है, जो उनके future को financially secure करता है।

Mutual funds for kids न सिर्फ wealth creation में मदद करते हैं, बल्कि आपको discipline और planning की habit भी सिखाते हैं। Compounding की ताकत और diversification के जरिए, आप छोटी रकम से भी बड़े goals achieve कर सकते हैं।

बच्चों का भविष्य secure करना हर पैरेंट का सपना होता है। Mutual fund portfolio के साथ आप यह सपना आसानी से पूरा कर सकते हैं।

आज ही 500 रुपये से SIP शुरू करें, और अपने बच्चे को financially strong future गिफ्ट करें। Financial planning जितनी जल्दी शुरू होगी, उतना बड़ा फायदा।

Call to Action: Groww, Zerodha, या mutual fund की official website पर जाएं, KYC complete करें, और अपने बच्चे के लिए पहला SIP शुरू करें।

छोटा investment, बड़ा future.

People also ask :

आप सिर्फ 500 रुपये महीने की छोटी रकम से भी SIP शुरू कर सकते हैं। ज़रूरी यह नहीं है कि रकम कितनी बड़ी है, बल्कि यह है कि आप कितनी जल्दी और नियमित रूप से invest शुरू करते हैं ताकि compounding का फायदा मिल सके।

बच्चों के लंबे समय के लक्ष्यों (10+ साल) के लिए Equity Mutual Funds (जैसे Large Cap या Flexi Cap Fund) और Aggressive Hybrid Funds सबसे अच्छे माने जाते हैं। ये फंड्स inflation को मात देकर high returns देने की क्षमता रखते हैं।

Investment शुरू करने की कोई ‘सही’ उम्र नहीं है, लेकिन नियम है – “जितना जल्दी, उतना बेहतर“। आप बच्चे के जन्म के बाद कभी भी शुरू कर सकते हैं, ताकि आपके investment को बढ़ने और compounding का फायदा उठाने के लिए ज़्यादा से ज़्यादा समय मिले।

बच्चे के 18 साल का होने पर उसका फोलियो ‘Dormant’ हो जाता है। उसे चालू करने के लिए बच्चे को अपना KYC (PAN, बैंक अकाउंट डिटेल्स) अपडेट कराना पड़ता है, जिसके बाद वह उस investment का कानूनी मालिक बन जाता है।

बिलकुल नहीं, बाज़ार गिरने पर SIP बंद करना सबसे बड़ी गलतियों में से एक है। गिरते बाज़ार में आपको उसी पैसे में ज़्यादा यूनिट्स मिलती हैं (Rupee Cost Averaging), जिससे लंबे समय में आपका रिटर्न और भी बेहतर होता है।

ज़्यादातर Children’s Gift Funds में एक lock-in period होता है जब तक बच्चा 18 साल का नहीं हो जाता। लेकिन अगर आप सामान्य Equity या Hybrid Fund में invest करते हैं तो ELSS (3 साल) को छोड़कर किसी और में कोई lock-in period नहीं होता है।